{kind=link}

- Get directions

- Leave a review

- Claim listing

- Bookmark

- Share

- Report

- prev

- next

- Tuesday, April 23, 2024 @ 11:00 am

In 2023, the Swiss biotech industry saw a record of CHF 7.3 billion in revenues recognized and was able to raise more than CHF 2 billion in capital investments - an increase of over 50% from 2022.

Frederik Schmachtenberg

EY | Partner, Global Health Sciences & Wellness Lead for Financial Accounting Advisory Services

Helena Rosa

EY | Senior Manager, Global Health Sciences & Wellness, Audit Services

During the course of 2023, the global biotech sector continued to suffer from developments that occurred over the past few years and some companies were even forced to stop operations. Especially in the United States, looking back, it became clear that several of the companies that went public through recent SPAC transactions were taken public too early in terms of their development stage.

In terms of biotech IPOs, the picture is mixed, with overall fewer IPOs happening, but this reduced count of IPOs raised more funds than in 2022. This is true both globally, where the IPO class of 2023 counted 18 IPOs (2022: 22) generating approximately USD 2.9 billion in funds (2022: USD 1.5 billion), as well as in the US with 16 IPOs (2022: 17) collecting a total of USD 2.6 billion (2022: USD 1.3 billion). The same is true for Europe, with only two biotech IPOs (2022: 5), raising USD 338 million (2022: USD 0.2 billion). Switzerland can be proud to have contributed one of these two European IPOs, as further detailed below.

Swiss biotech landscape

In 2023, the Swiss biotech industry saw new records in terms of revenues recognized (CHF 7.3 billion in 2023 compared to CHF 6.8 billion in 2022), whereas R&D investments slightly decreased (CHF 2.4 billion in 2023 compared to CHF 2.7 billion in 2022). Despite a slight decrease in R&D expenses, the number of FTEs working in Swiss R&D biotech companies remained almost unchanged in 2023 compared to 2022, which seems to indicate that, even when some companies have to restructure or reorganize, the highly qualified employees often find new opportunities with other companies in the sector.

Swiss biotech financing

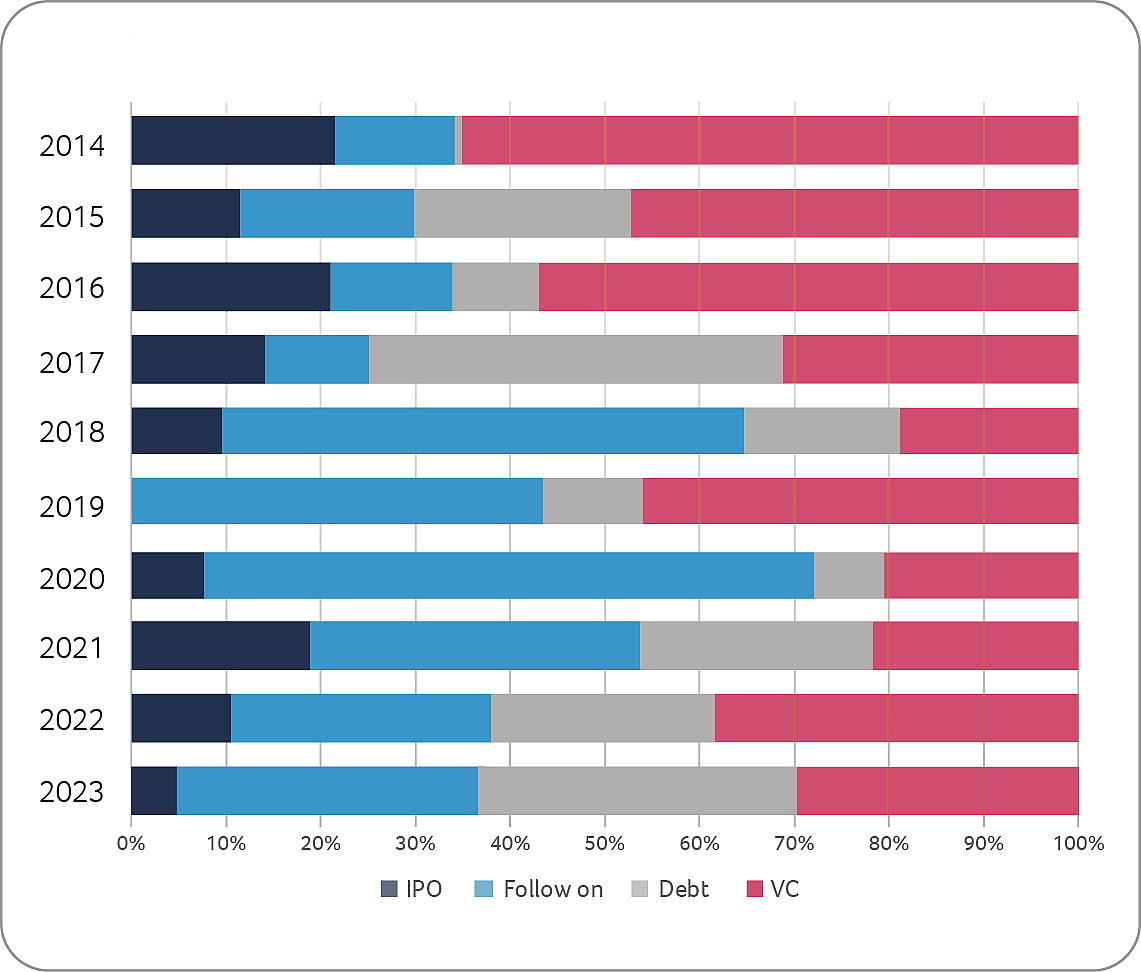

Despite the above-mentioned challenges, the Swiss biotech industry was able to raise more than CHF 2 billion in 2023 (2022: CHF 1.3 billion), an increase by more than 50% in capital investments compared to 2022, with around CHF 1.4 billion collected by public companies and the remaining CHF 0.6 transactionsbillion collected by private companies. Noema Pharma with CHF 103 million raised, and Alentis Therapeutics with CHF 94 million raised, were the two largest private company financing transactions in 2023.

The only Swiss biotech company that went public in 2023 was Oculis, with a SPAC transaction on NASDAQ, which was initially started in late 2022 and successfully completed in March 2023, collecting gross proceeds of USD 104 million, plus a follow-on financing with another USD 40 million raised in May 2023.

Further, MoonLake Immunotherapeutics, one of the two Swiss biotech companies that went public in 2022, due to some positive clinical results in 2023, was able to gain additional funds from investors through a follow-on transaction as well as from a market-share program (totaling approximately CHF 415 million).

However, 2023 was also a difficult year for several companies, which led to the fact that some restructuring measures had to be initiated or, even worse, the going concern assumption was in question due to setbacks in clinical studies or insufficient funding. Selling of valuable assets (Evolva, Spexis), entering a reversemerger transaction (Kinarus), or even taking the decision to stop operations (ObsEva) were some of the unfortunate implications.

In summary, while total capital investments in 2023 increased by more than 50% compared to 2022, it was not a high count of companies that benefited or, in other words, many companies unfortunately received very little or no funding. This is also evidenced by the fact that the average financing of the Top 5 financing transactions in 2023 increased by 42% for public biotech companies and by 44% for private biotech companies, compared to 2022.

In addition, or one could say as a result, with equity and debt markets still being more difficult to access for many companies, Swiss biotech companies continued to be agile in terms of finding alternative ways of financing (licensing, collaborations, but also monetization of assets transactions) which, in a similar way to 2022, provided non-dilutive financing also in 2023.

M&A and collaborations

Swiss companies were involved in several significant M&A transactions:

- Bruker acquired a majority stake in Biognosys

- Siegfried acquired a 95% stake in DiNAMIQS (subsidiary of Dinaqor) as a best-in-class development and manufacturing platform for cell and gene therapies

- Ironwood Pharma took over VectivBio for more than USD 1 billion

- Abiogen Pharma acquired 97.09% stake in EffRx Pharmaceuticals

- Idorsia sold its Asia Pacific (ex-China) operations to Sosei Heptares for a total consideration of CHF 400 million

- Pierre Fabre Laboratories purchased Vertical Bio and its innovative targeted therapy candidate for patients suffering from non-small cell lung cancer with MET alteration

- Boehringer Ingelheim acquired T3 Pharma for an amount of up to CHF 450 million

- Evolva and Lallemand closed the sale of Evolva AG to Danstar Ferment AG

At the same time, entering into new collaboration and licensing agreements was important for several Swiss biotech companies as some of those partnerships contained significant attractive financial components, which – as mentioned above – provided alternative ways of funding (alternatives to equity or debt financings, which continued to be more difficult to obtain in 2023). A selection of such collaboration and licensing transactions is shown below:

- EraCal and Nestle Health Science entered collaboration to develop new anti-obesity treatments

- STALICLA partnered with US National Institute on Drug Abuse for Phase III development of anti-cocaine drug mavoglurant

- CRISPR Therapeutics closed licensing deal with Vertex worth up to USD 330 million for hypoimmune cell therapy development

- Santhera closed exclusive North American license agreement with Catalyst Pharmaceuticals for vamorolone worth up to USD 231 million plus royalties

- Relief Therapeutics announced USD 46.5 million license agreement for OLPRUVA™ (ACER-001) for urea cycle disorders with Acer Therapeutics

Product developments

In 2023, the industry saw a similarly high number of regulatory approvals compared to prior years, which is positive. More specifically, the EMA approved 77 new drugs in 2023 (2022: 89 new drugs) and the FDA approved 55 new drugs (compared to 37 in 2022).

Furthermore, among the new FDA approvals there were two new drugs developed by Swiss companies. Santhera Pharmaceuticals received approval for AGAMREE® (vamorolone) for the Treatment of Duchenne Muscular Dystrophy (DMD). Further, the FDA approved the CRISPR/Cas9 gene-edited treatment, co-developed by CRISPR Therapeutics and Vertex Pharmaceuticals, in sickle cell disease. Both drugs were afterwards also approved by European authorities.

The level of approvals by Swissmedic was slightly above prior year with a total of 49 new drugs (2022: 47).

Awards

Several Swiss biotech companies also received various prestigious awards throughout 2023. Some of these awards included:

- 2023 Swiss Digital Innovation of the Year award for Tigen SA

- Luca Santarelli, CEO of VectivBio until June 2023 when VectivBio was acquired by Ironwood Pharma, received Entrepreneur of the Year (EoY) award in the category “Industry, High-Tech & Life Sciences”

- Jenny Prange and Deana Mohr, Co-founders of Muvon Therapeutics, share Swiss Female Innovator of the Year Award

- Top 100 Startup Awards: HAYA Therapeutics wins the first prize

Private & public Swiss biotech regional financing 2021-2023